I was standing in the TSA line at Logan Airport recently when I looked up and saw the championship banners hanging overhead. Like most Boston sports fans, I felt a little pride. But it also got me thinking about something else entirely: investing. As a family financial planner, it’s hard to turn off that side of my brain, regardless of where I am!

Today, it’s easy to look at Boston sports and assume success was inevitable. The Patriots, Red Sox, Celtics, and Bruins have delivered championship after championship over the last twenty-five years. But anyone who lived through the late 1980s and 1990s remembers a very different story.

Between the Celtics’ championship in 1986 and the Patriots’ first Super Bowl in 2001, Boston fans endured years of heartbreak and disappointment (decades upon decades with the Sox to that point). There were plenty of opportunities to give up.

If you had, you would have missed one of the greatest championship runs any sports city has ever experienced, and that same lesson applies to investing.

The Hardest Part Is Staying Around Long Enough

One of the challenges of investing is that downturns feel permanent when you’re living through them. During bear markets, every headline seems negative, and every forecast becomes more pessimistic. Every decline feels like evidence that this time is somehow different. But history tells a different story.

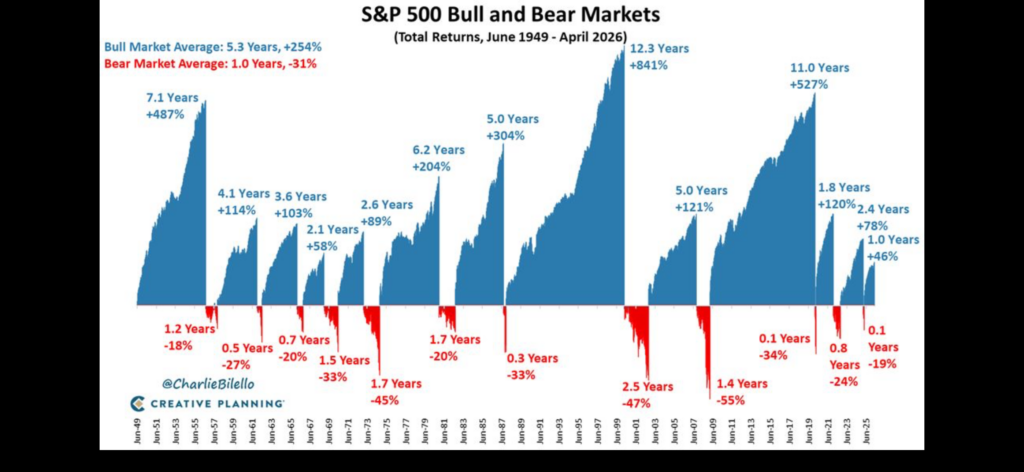

Looking at market data going back to 1949, the average bear market lasted about one year and declined roughly 31%. That’s certainly painful, and nobody enjoys living through it. However, the average bull market lasted more than five years and returned over 250%.

But here’s the problem: you only benefit from those long stretches if you’re still invested when they arrive!

The Sequence of Return Risk – Explained

What makes the current Boston sports slump easier to stomach, at least a little, is perspective. If all four teams had been this frustrating back in 2001, before the Patriots, Red Sox, Bruins, and Celtics spent two decades hanging banners, it would have felt very different. But after watching one of the greatest championship runs any sports city has ever had, a rough stretch lands with a little less emotional force. That doesn’t mean fans enjoy it; it just means the context matters! A drought after years of winning feels different than a drought when you’re still waiting for the first breakthrough.

Keeping this type of perspective is how savvy investors view market fluctuations in relation to where they are in life: “sequence of return risk.” A bad market stretch doesn’t hurt everyone the same way; it depends on when it shows up.

For example, a bear market at age 65, right as someone retires and starts drawing from their portfolio, can be far more damaging than the same downturn hitting at 75, when they’re already 10 years into retirement with a plan in place. Timing matters. The order of good years and bad years matters.

In the same way Boston’s current sports “mess” feels more survivable because of the banners that came before it, market losses also land differently depending on where you are in your financial timeline and what kind of cushion or flexibility you’ve already built.

Staying Invested During Market Volatility – The Lost Decade Didn’t Stay Lost

Many investors remember the period from 2000 through 2010 as the “Lost Decade.” The dot-com bubble burst. Then came 9/11. Then the financial crisis. It felt like every time markets gained momentum, something knocked them back down. For investors living through it, it was easy to wonder whether the market would ever produce meaningful returns again.

We Boston sports fans experienced something similar. Every season began with cautious optimism and ended with another painful lesson in disappointment. If you judged the future solely based on what had happened recently, giving up almost seemed reasonable, but both stories eventually changed.

The decade following the financial crisis produced one of the longest and strongest bull markets in history. From 2009 through early 2020, the market gained more than 500% over eleven years. Investors who sold during the crisis missed much of that recovery. Likewise, Boston sports fans who checked out around 2000 missed more than twenty championships across the four major sports! Yes, that really happened.

Bear Markets Make Headlines. Bull Markets Build Wealth.

One thing that stands out in market history is how differently we remember gains and losses. We vividly remember 2008 and March 2020. We remember inflation scares, banking concerns, and recessions. What we often forget is how much longer markets spend moving higher than they spend moving lower.

The chart of market history looks intimidating because the declines are sharp and dramatic. But when you step back, you notice something else: the blue sections are much larger than the red ones. The declines get all the attention, but the recoveries create the wealth. That’s why successful investing often has less to do with predicting the next move and more to do with surviving the difficult stretches.

Staying Invested During Market Volatility – What Winning Actually Looks Like

When people look at successful investors, they often assume the difference is intelligence or finding the perfect stock. In reality, it’s usually endurance. The investors who succeed are often the ones who stay committed when others become discouraged and understand that temporary setbacks are part of the process.

Nobody knew in 2001 that a man named Tom Brady would get his big start or that the Red Sox were on the verge of breaking a lingering curse that had lasted for nearly a century. The city was about to begin one of the greatest championship runs in sports history. If you had given up on Boston sports during the drought, you would have missed decades of unforgettable moments. If you had sold everything during the financial crisis of 2008, you would have missed one of the strongest bull markets ever recorded. That’s why I spend so much time talking about plans rather than predictions.

Remember, the next championship banner doesn’t go up during the losing streak, and the next bull market doesn’t begin when everyone feels confident. Both usually arrive when people are starting to wonder whether it’s worth sticking around, and that’s often when sticking to the plan matters most.

Let’s discuss your plan.