The 50/30/20 rule: spend 50% on needs, 30% on wants, and save 20% for the future. It’s clean and easily digestible; it feels like the kind of structure people crave. I understand the appeal as it simplifies something that often feels overwhelming. However, real life rarely fits inside clean percentages.

Simple rules like the 50/30/20 rule can be good starting points. They raise awareness and provide a baseline for thinking about spending and saving habits. They offer very casual building blocks and parameters to consider, but the trouble arises when they are treated as personalized financial plans rather than general guidelines.

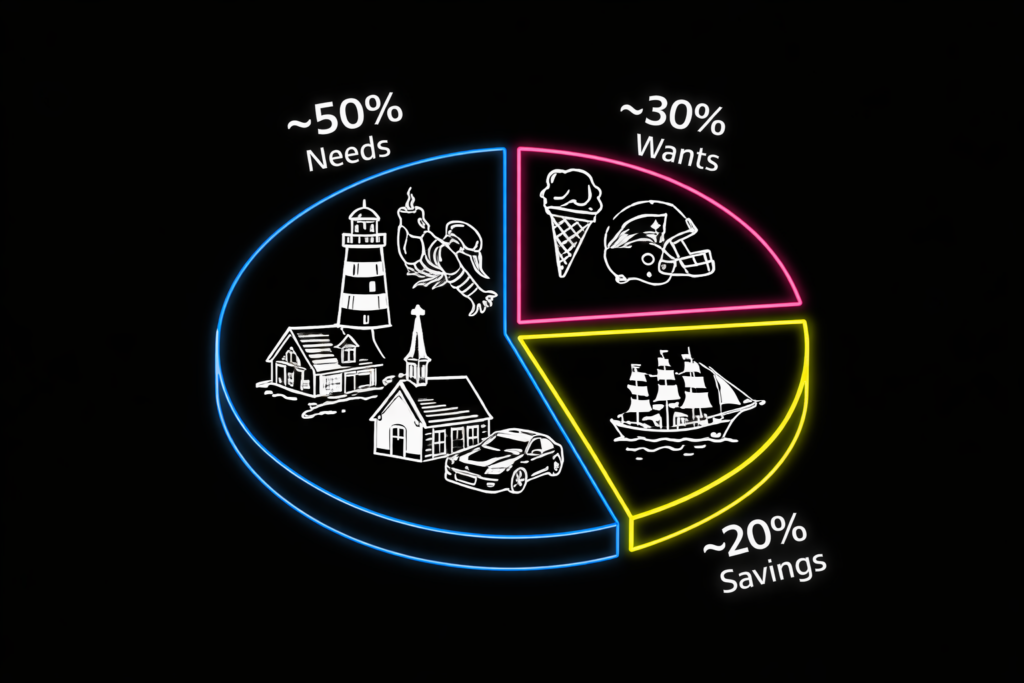

Why the 50/30/20 Rule Works in Theory

Your income/family size/career stage all shape what’s realistic. Someone early in their career, renting an apartment with minimal obligations, has more flexibility than a couple managing a mortgage and aging parents simultaneously. What works in your 20s often looks completely different in your 40s or 50s.

Here’s a big knock against rules like this: fixed percentages ignore timing. Life has seasons, and there are seasons when spending rises, like when buying a home and raising young children. There’s a season to fund education, and seasons when saving accelerates. Trying to force a rigid formula across every life stage usually doesn’t work and makes people feel like they’re failing when they’re not.

Remember, enjoying times with your young kids at Disney World and not skipping the memories isn’t failing; it’s embracing a fleeting point in life. A financial plan only works if you can live with it over time.

Small Wins Change Momentum

The tension between optimization and behavior shows up constantly in personal finance discussions. The most technical plan doesn’t always produce the best outcome if it is too rigid to follow; as humans, we need to feel progress to keep momentum going.

Think about this scenario: should you pay off your smallest debt first or your largest? Mathematically, tackling the highest-interest balance makes the most sense. But behaviorally, small wins create motivation. Seeing progress keeps people engaged and working towards financial goals.

A recent discussion on Freakonomics Radio explored how financial rules tend to prioritize mathematical precision over human behavior. The takeaway was simple: people don’t stick to perfect formulas; they stick to plans that feel achievable. It keeps people moving forward long enough to see long-term results.

We’re not bots, and we need to feel gains to keep moving along!

Spending Isn’t Always The Biggest Sin

One of the biggest pitfalls of rigid budgeting frameworks is the pressure they create. I’ve seen families try to save so aggressively that they make their plan unsustainable. Eventually, burnout sets in.

Childcare and nannies, housing costs, these aren’t discretionary luxuries for many families. They’re structural expenses tied to career and life stage. Beating yourself up because you don’t neatly align with the 50/30/20 rule won’t help you or your family. The more important question is whether the fundamentals are in place: Do you have liquidity? Are you building savings consistently? Is your mortgage structured appropriately for your time horizon/risk tolerance?

Now, don’t think I’m saying that adjustments shouldn’t happen. If you’re off track, there are often simple levers to pull. Maybe discretionary spending gets dialed back, and some indulgent habits are modified. Still, those changes should be thoughtful and intentional, not guilt-driven reactions to a rule that never fully fit your situation to begin with.

Finding A Plan That Fits Your Life

The 50/30/20 rule can provide perspective for starting big financial conversations. But it shouldn’t define the strategy; real family financial planning adapts to the life you’re living.

As a family financial advisor, my take is this: a flexible plan you can sustain will always outperform a rigid one you abandon. If you’d like to talk through what your allocation should look like based on your life stage, responsibilities, and long-term goals, I’m always happy to help, and my door is always open.